27 Nov BIG BAD WOLF (LONG-TERM CARE COSTS) CAN’T BLOW DOWN HOUSE MADE OF IRREVOCABLE TRUSTS

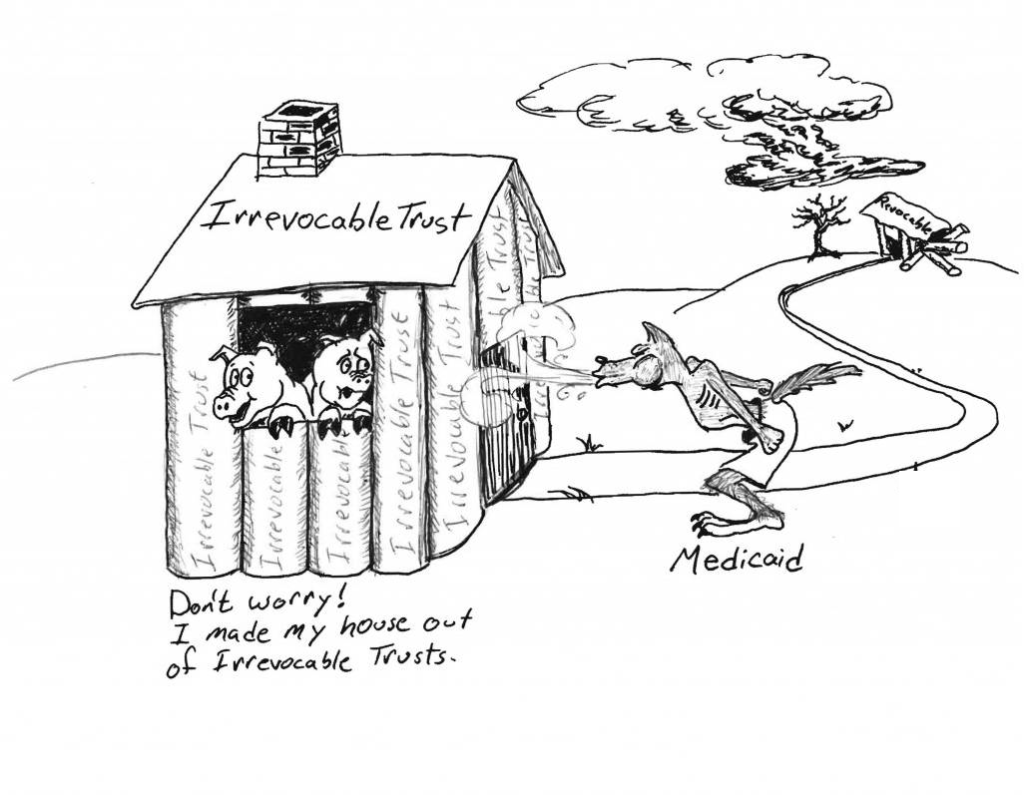

Irrevocable trusts are a tool commonly used by many who plan in advance to preserve resources if they desire governmental assistance to pay for long-term care costs. Although Americans are living longer resulting in increased need for long-term care, sales of long-term care insurance have dropped tenfold. Furthermore, most Americans have inadequate assets or income to be self-insured for long-term care costs and Medicare has very limited coverage. Additionally, some simply can’t afford long-term care insurance premiums or they can’t pass underwriting.

Medicaid helps pay for long-term care costs – but it is “means-tested” as an applicant generally must have limited resources for eligibility. Since the government anticipates potential applicants to make gifts or uncompensated transfers to reduce assets to be eligible, the government has a five year “look-back” period. In other words, if the long-term care Medicaid applicant made a gift or uncompensated transfer (subject to limited exceptions) within five years, then the government presumes it was purposefully done to reduce assets so that the government would help pay for the costs. Notwithstanding the look-back period, many plan in advance by using certain types of irrevocable trusts to protect resources from Medicaid “spend down”. Furthermore, even though transfers are subject to the five year look-back period, it doesn’t mean there are five years of ineligibility. Sometimes actions can be done to eliminate or reduce the transfer penalty. Usually the trust is designed so the trust is tax-neutral. However, Medicaid rules prohibit the Medicaid applicant from being a beneficiary of the principal of the trust. On the other hand, the Medicaid applicant can retain the power to change beneficiaries (as long as they cannot change the beneficiary to the potential applicant which includes the applicant’s spouse). Since the trust is irrevocable, it is considered a transfer subject to the five year look-back period for long-term care Medicaid. Many states do not permit the applicant to be the trustee of the trust.

In addition to protecting assets from Medicaid “spend down”, the trust generally gives creditor protection for the assets held in the trust. Furthermore, assets held in the trust avoid probate and the trust can be designed to protect beneficiaries from: (a) creditor issues, (b) being a spendthrift, (c) being disabled, (d) bad marriages; and (e) make certain the assets are invested and distributed the way the trustor desires, etc. It should be mentioned that the type of irrevocable trust used in planning for Veteran’s benefits (which has a three year look-back period) is different than the ones traditionally used in planning for Medicaid benefits. There are numerous types of irrevocable trusts. Like all estate planning, irrevocable trusts are simply one of the tools in the toolbox used to achieve the goals of the client.

If interested in learning more, consider attending our next free “Estate Planning Essentials” workshop by calling us at (214) 720-0102 or sign up by clicking here.